Last Updated: February 10, 2021

By Andrew Duguay, Prevedere Chief Economist

Data updated: June 24, 2020

If COVID-19 cases were declining as rapidly as we’d like in the U.S., we wouldn’t still be talking about this pandemic when discussing economic recovery. Instead, we would be focusing more on economic recovery factors alone. Let’s ponder what reopening and economic recovery look like, given the current pandemic effects in the United States.

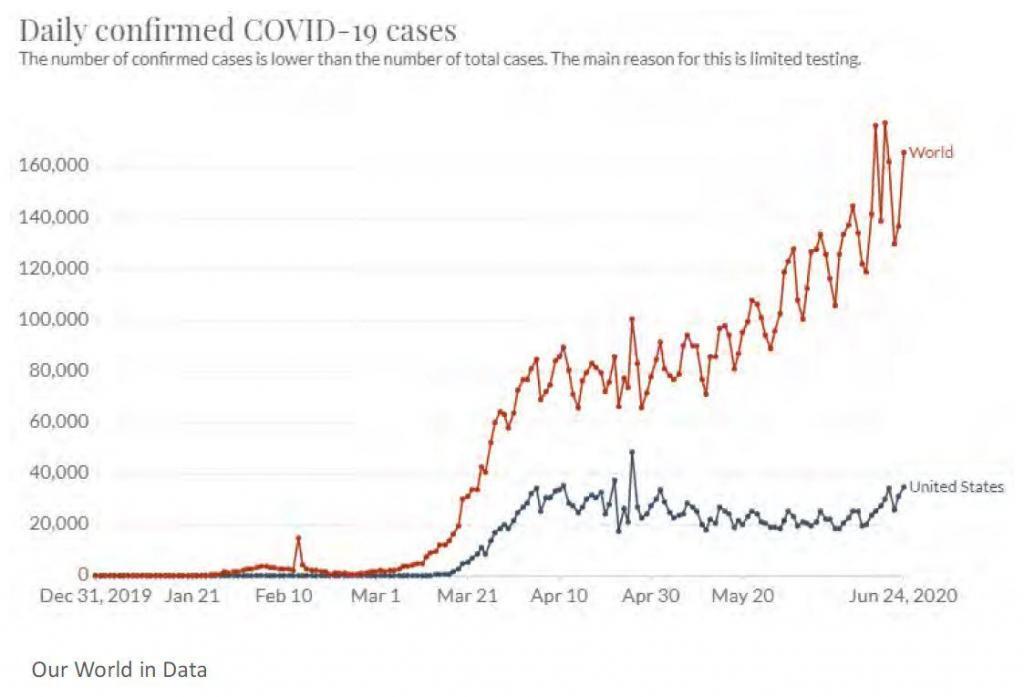

What we’re seeing is that the latest data is complicated. June 23rd tracked as the fourth worst day for the number of new coronavirus cases in the United States, and this was the newest cases in a single day since April 26th. That peek is represented on the blue line in the graph below.

Worldwide the coronavirus is still spreading and especially continues to gain momentum in emerging markets. We observed from increases in COVID-19 cases from Asia to Europe that peaks in cases often triggered strict shutdown efforts. In the United States, our projections for economic recovery are largely based on a steady decline in overall cases. This has led to forecasts of continued economic recovery in the second half of the year.

Worldwide the coronavirus is still spreading and especially continues to gain momentum in emerging markets. We observed from increases in COVID-19 cases from Asia to Europe that peaks in cases often triggered strict shutdown efforts. In the United States, our projections for economic recovery are largely based on a steady decline in overall cases. This has led to forecasts of continued economic recovery in the second half of the year.

So what does this equate to for our domestic economic outlook? We expect some volatility in the coming months. Comparing this against what seems to be positive news coming out of the economic sphere can be confusing. Let’s touch on the ramifications as we’re seeing a lot of positive financial numbers lately that might give us some inclination that the worst is over and better days are ahead.

There will be a summer of volatility in the United States because we see continued increases in the coronavirus cases. Economists attempt to bring some certainty to the economic discussion, and that’s why we continue to dialogue about the nuances within this unprecedented road to an exceptional economic period.

COVID-19 Risks this Summer

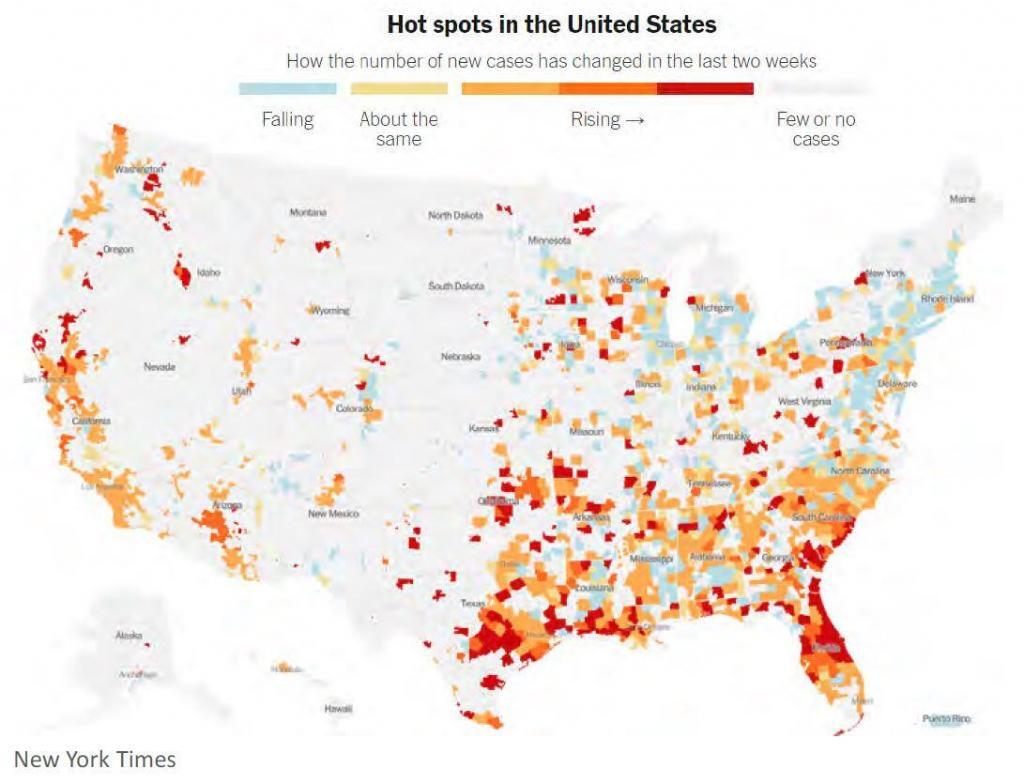

The map above is showing where cases are increasing in the orange and red versus decreasing in blue, and there’s a lot less blue than even last week when I showed this chart. To put this in numbers, 27 states are seeing increased COVID-19 cases, while 14 states are just seeing stability.

Only 12 states and the district of Columbia, are experiencing a decline. The complex viral caseload is in contrast to the fact that every state has in the process of reopening.

Are we gonna have to consider mandating quarantine or closing businesses, what could this signify for the economy? There are reasons to be cautiously optimistic because at least nine states make that list of infection rates above 10%, which is criteria to cause them to go into quarantine potentially.

Determining a quarantine order is largely left up to states. However, once we start to see states moving more towards the protective measures that restrict economic freedom, this is a cause for economic recovery projection concern. Some of the positive numbers that we are seeing in May as businesses are opening up and starting to extrapolate into June, might start to reverse again. Adding to this is the fact that we still have over 20 million continuing jobless claims in the United States… we’re far from out of danger

Improving Economic Conditions

The retail sales number was headlining as very strong in May and June from advanced retail sales sourced from the Census Bureau. The growth caught people by surprise, and the headlines read there was a 17.7% jump. The most significant monthly jump ever in the U.S. as consumers were going back and spending, and the stock market loved it.

The numbers shown in the chart obviously show abnormally strong growth. However, we need to take this news into context. In May, multiple issues were happening simultaneously. The nation was recovering from a very weak April. When economists look at data in the midst of volatility, we aim to determine what the data is telling us, and it helps to smooth out volatility using moving averages.

The other thing we have to consider is that there was a record jump in incomes in April largely due to the combination of stimulus checks and the fact that the federal government expanded the unemployment benefits. This combination led to 40 to 50% of people who lost their jobs, taking in more income under benefits than before losing their jobs, which is very generous. This could cause a spending surge and we have to keep our eye on that. When there is sudden extra income and extra time, consumers are likely to spend. When considering this information, we understand that the main number didn’t jump, so is this a net positive?

Let’s take a different perspective. The May retail sales headline said 17.7% jump on a period-over-period percent change, seasonally adjusted annual rate. From an economist’s perspective, it is essential to step back and look at a year-over-year basis. When you get down to the ‘nitty-gritty’ of forecasting and planning for your business, this becomes even more imperative.

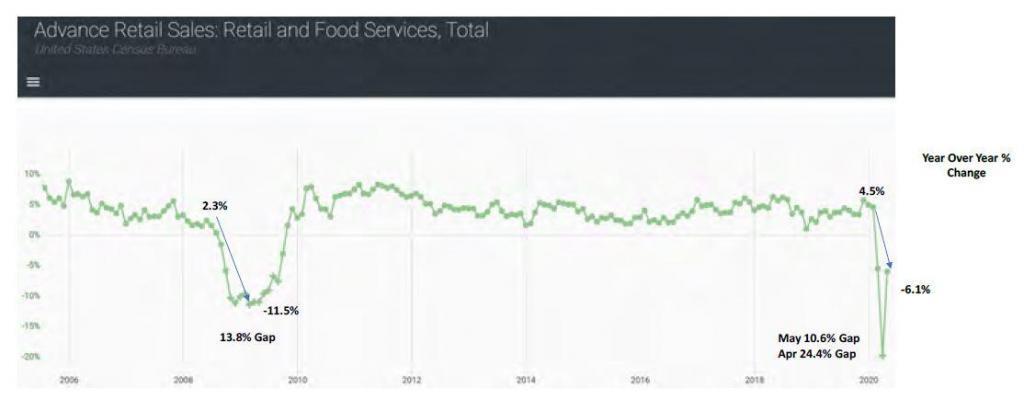

Looking at the numbers beyond the headlines gives us some additional context. Is this better than anything we have ever seen, or just better than a poor performing April? So let’s look at the same dataset on a year-over-year basis. And what we see is that on a year-over-year basis, retail sales in May are still down. They’re down 6.1%. This qualifies as the second-worst number on a year-over-year basis since the last recession. Now let’s look at the last recession for additional context in the chart below.

In the last recession, we saw that cyclically, we were growing at about 2.3% on a year-over-year basis in retail sales. Over the course of a few months, things bottomed out around -11.5%. If you look at where we were before COVID, where retail sales grew at 4.5% and then declined to -6.1, that’s a 10.6% gap. This actually aligns closely with the ‘peak to trough’ of the last recession, at 13.8%, which is still a very drastic change in retail spending.

This still does not look good by any measures. Of course, when compared to April, where everything was literally shut down, that was a record-breaking decline. And that was also a much more significant gap than what we experienced in the last recession. What we’re seeing is recovery from very adverse conditions. Not necessarily a new happy spending consumer.

Consumers are still hesitant. We have talked a lot about consumer sentiment data over the last few weeks. And if you look at this on a year-over-year basis, you see that consumers are overall conservative, just not as negative in April. This also makes logical sense, given most of the economy was wholly shut down in April.

So the rise of new COVID-19 cases brings some elevated risk that we don’t want to realize. Are we going to shelter in place in the upcoming months? That remains to be seen and is subject primarily to the health crisis itself.

Looking At The Data like an Economist

So when looking at economic leading indicators, consider them from a year-over-year perspective, even if the media quotes a period-over-period statistic.

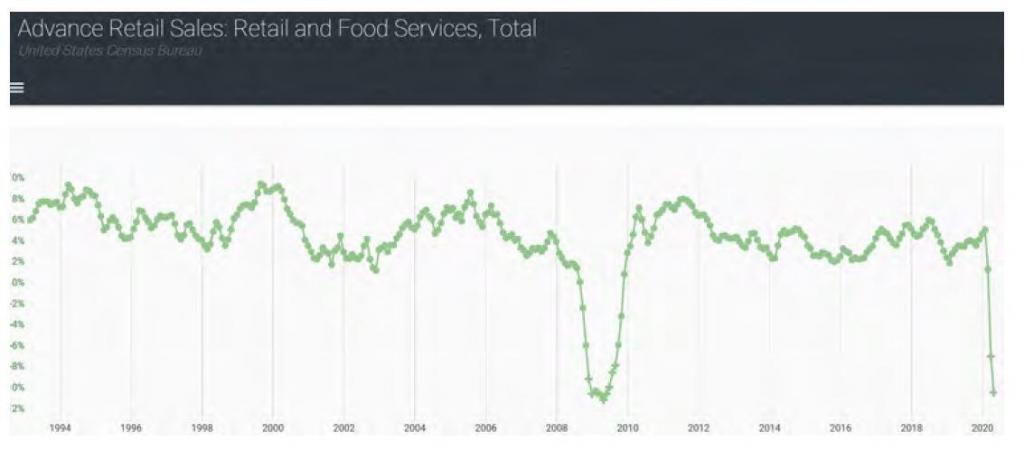

This method was highlighted by Joe Ellis, a Wall Street veteran, in his book, Ahead of The Curve. He advised to look at moving averages’ year-over-year growth rate. This is how we do some of our predictive modelings at Prevedere, looking at the three-period moving average, year-over-year growth rate. So let’s look at the same data set when we apply a three-period moving average. A moving average is meant to smooth out some month to month volatility, which we see a lot of right now.

When you look at the very far right side of this chart, you see that this looks a whole lot like the worst recession we’ve seen–The Great Recession. Even with the primary data, things don’t look much better than they did back then. And the economy was very weak at the time, taking a long time to recover. Just keep that in perspective, what could look like a headline recovery put in a broader context, smoothed over with moving averages, shows you that we still have a long way to climb out of this recession.

Why did people think the recently reported number was so positive? It wasn’t that the main number was actually so good in itself; it was the fact that economists when surveyed, were expecting something far worse. Economists were expecting growth. They expected 9% growth and actuals came in at 17.7%. Perspective like this is essential. And if the markets were trading on some expectation that retail sales in May we’re going to rise 9%, but they rose 18%, that was viewed as a positive economic surprise. There are measures of this, with one of those being the Citi Group economic surprise index.

The Citi Group economic surprise index has been at record-breaking levels of recent. Because the data is so volatile, they have a hard time modeling and understanding just what each dataset is going to reveal. An industry secret; given that we have a record-breaking stimulus, combined with record-breaking job losses, life is very difficult for economists. The environment has changed.

It’s tough to know precisely on a month-to-month basis what numbers are going to be. This creates immense volatility in the marketplace. When we see the numbers, it’s not the fact that they are positive, it is the fact that they were better than economists were forecasting because they are thinking more pessimistically.

Forecasting Accuracy

So what does this all mean for planning your business? Don’t rely on just a single indicator. You will need to look at a broad set of indicators to plan the second half of the year effectively. And you are going to need to come up with multiple scenarios for how the economy will recover. You need to insulate your business, considering the amount of volatility we face.

So single-point forecasts, relying on one indicator, whether it’s oil prices or housing starts, that go-to indicator your business might have looked at in the past, is no longer good enough. You will need to have a thorough understanding of a broad set of indicators to start diagnosing economic conditions.

Organizations should consider moving averages and take signals into a broader context. If you just focus on a single month from a single data point, you could have a vastly skewed perspective where the economy is at any given moment. So look at multiple indicators, utilize things like working on a year-over-year or moving average.

And make sure that you come up with multiple plans for the future and the second half of the year versus single-point forecast. This is an integral part of how we encourage our customers to respond, recover, and thrive in the new COVID-19 environment.

Planning and forecasting based on historical performance are no longer valid in today’s economic climate. As you look ahead beyond the immediate crisis and consider your business plans, having visibility to external economic factors and considering how your company will fare in the “new normal” economy is paramount.

It is one thing to spend a lot of time and effort to build a plan that provides a scenario for today. But during times of uncertainty by definition, that plan is highly likely going to be wrong. So, the ROI on multiple scenarios forecasts is going to be based on how adaptable models are to potentially changing conditions. To build a single static dimension of factors will only be as good as the actions immediately indicated from that plan.

When building models, build to adapt to new information. Businesses that can incorporate the latest information to scale with varied outputs become repeatable and adaptable to new facts and data as they are released. For instance, your organization may be prepared in advance of an announcement of extending government stimulus.

This will help your business to adapt. Because during a business cycle low, this is often the most critical time for a company. It’s not just an act of survival, but it’s actually an act of changing your company. During business-cycle lows is when you can often lock in and find more critical talent and build up competitive edges. If you’re adapting to the new normal faster, this could be creating more market opportunities for you. Remain open to thinking there is a considerable business opportunity during a weak time in the business cycle, particularly. And so the best businesses will try to take advantage of that part of that is having adaptable planning given the fact that there’s so much uncertainty.

Complimentary Economic Leading Indicator Access

As the U.S. transitions into the recovery phase of the COVID-19-induced recession, it is more important than ever to have access to timely, reliable data and expert economic analysis to help guide forecast decision making and re-planning. To meet this need, Prevedere has created a complimentary Economic Outlook Weekly report.

The report provides executives with leading indicators to watch that offer an unbiased view of the evolving economic landscape. The Economic Outlook Weekly report is emailed weekly and includes a range of demand and supply-side factors to cover the full spectrum of economic activity. Each indicator is displayed graphically and updated automatically as new information is released. There is no charge to receive this service. Sign up for your complimentary access here.

Complimentary Economic Outlook Weekly Services Include:

• Macro view of key recession economic indicators

• Regular economist reports offered as information becomes available

• Weekly updates to your inbox