Last Updated: February 10, 2021

By Andrew Duguay, Chief Economist

Data updated: June 1, 2020

Many states are continuing to slowly turn the dial on reopening the U.S. economy, with all 50 states resuming operation in some capacity. As the U.S. transitions into this second phase of the COVID-19induced recession, how fast people can get back to work and realize some sense of normalcy will likely shape the U.S. economy this summer.

Impact of New Global COVID-19 Cases on Recovery

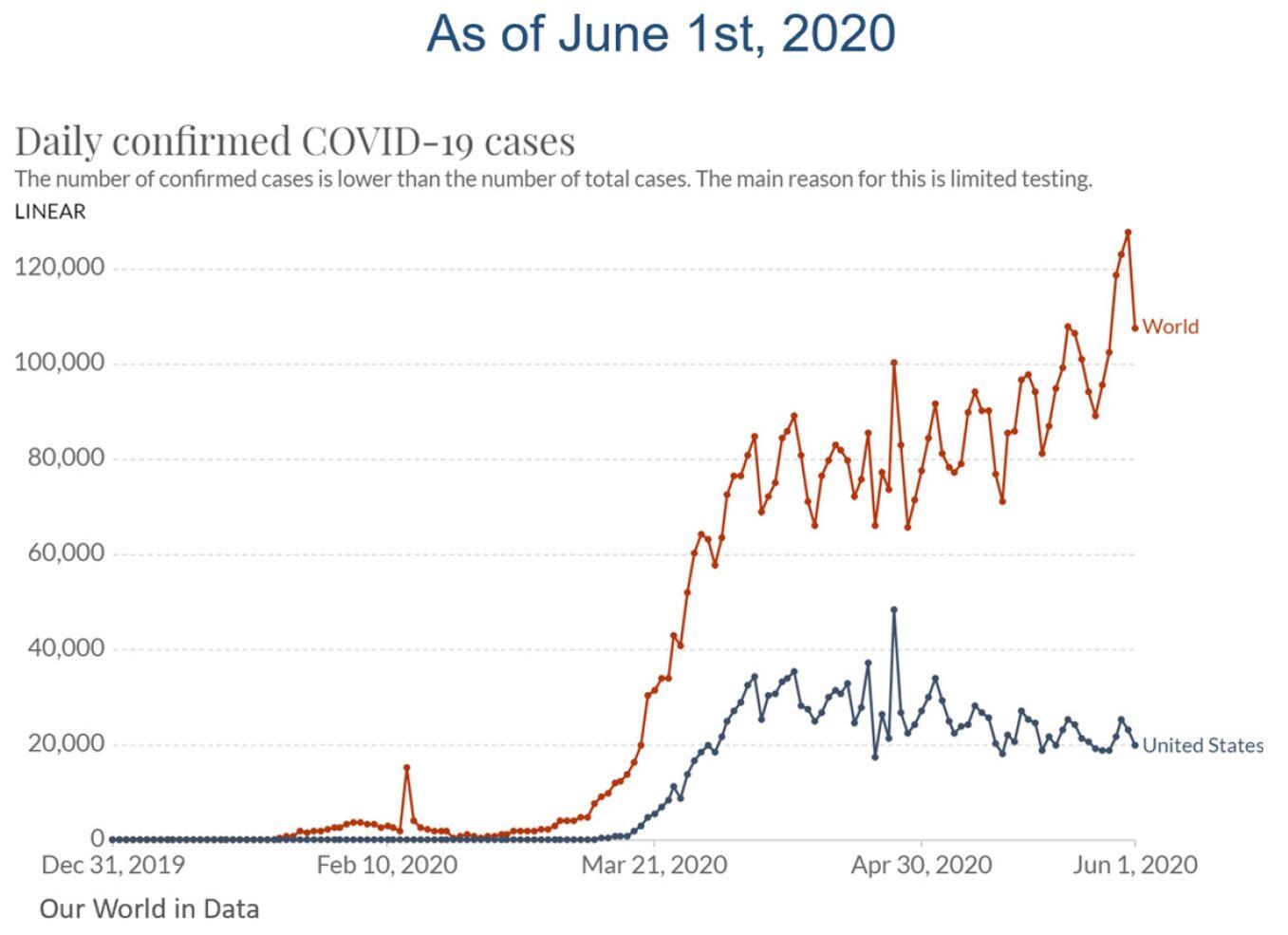

As witnessed, the pandemic itself can dictate the health of the economy. Important variables in the recovery include uncertainty around whether states will stay open if there is a spike in cases and if people will even feel safe to resume somewhat normal activity. Just a few weeks ago, there was optimism that perhaps the number of new cases globally had peaked. However, over the past couple weeks there has been an upward trend in global cases, primarily from emerging markets where new cases have appeared in places like Brazil and India. But as testing capacity increases, the U.S. is still very much contributing towards the total number of new cases.

As indicated in the chart above, the United States is really no better off than it was just a few weeks ago in total number of new cases daily. Ideally, this line would be decreasing at a faster pace; bending the curve downwards rather than continuing a horizontal track.

This becomes much more noteworthy as businesses start to reopen, posing renewed threats as people relax their social distancing. And while the economy desperately needs businesses to reopen and for people to get back to some form of normal in terms of their activity, maintaining safety measures is necessary because of the potential of a second wave of coronavirus cases.

The U.S. is not really any safer today than a few months ago, yet some of the restrictive measures have been relaxed. New cases remain at elevated levels. The reopening of businesses poses new threats because infection levels have not markedly decreased.

These factors give us pause and inform our projection of a U-shaped recovery, which is still a broad projection. While the second half of the year will be better than the first half and the slow recovery will extend into 2021, there’s still considerable downside risk.

There is no vaccine or cure for COVID-19, and the number of cases remain at an elevated level. As long as these two facts persist, there’s a strong possibility that the economic outlook may need to be adjusted, potentially downward, as the situation unfolds.

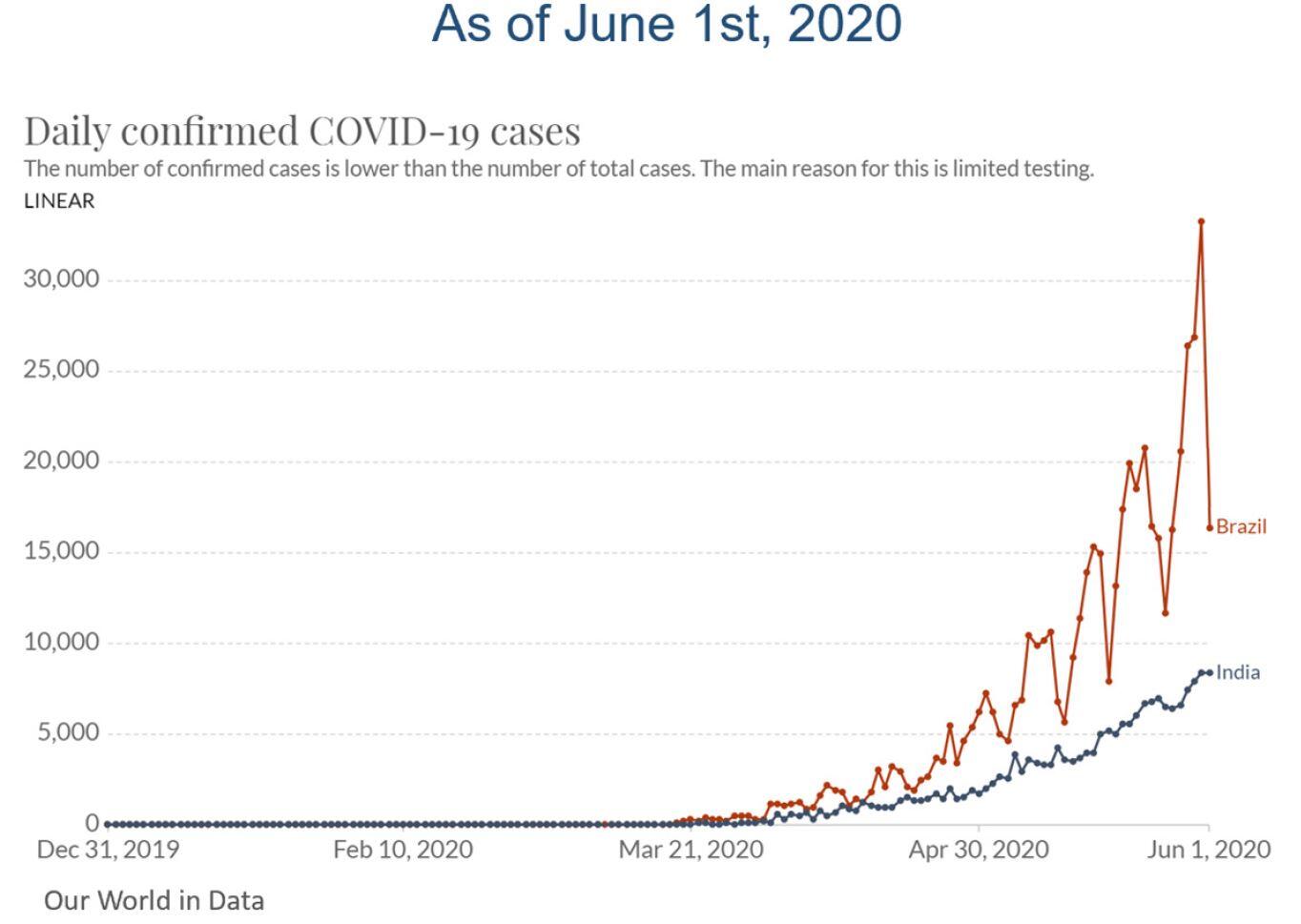

In looking at new COVID-19 cases outside of the United States, countries such as Brazil and India are not over the curve— and seeing a decrease in cases. In fact, a rapid rate of increases in cases in these countries are driving the total world count to climb over the last few weeks.

Stemming from Asia where countries had a good amount of testing, the coronavirus challenged the U.S. and Europe’s testing capacity, and albeit slow at first, testing ramped up quickly due to advancements made by the United States.

COVID-19 migrating to emerging markets where many of these countries lack strong resources resulting in weaker testing, poses two risks. The first risk is that these populations may not fully realize the possible impact of COVID-19 and they may not restrict their movement soon enough, especially when lack of testing can’t reveal outbreaks.

The second risk is that the ability to ramp up and execute testing in these countries is a much more complex task than it is in developed nations. As the coronavirus pandemic shifts its peak toward emerging markets, we will likely see more uncertainty in the data. But even with reporting inconsistencies, there still appears to be alarming levels of new cases. Obviously, this migration is damaging to the local economies, but it is also a reminder that there should be continued caution all around the world because the pandemic hasn’t disappeared; it’s just shifting countries.

Impact of Stimulus on Income and Recovery

Some companies are undoubtedly feeling the effects of coronavirus, but others may be surprised by the lack of decline in their business given the circumstances. Many retailers have posted quite solid numbers. In the U.S., this is likely due to not having ever experienced something of this scale—not only a health crisis but a government response of such magnitude.

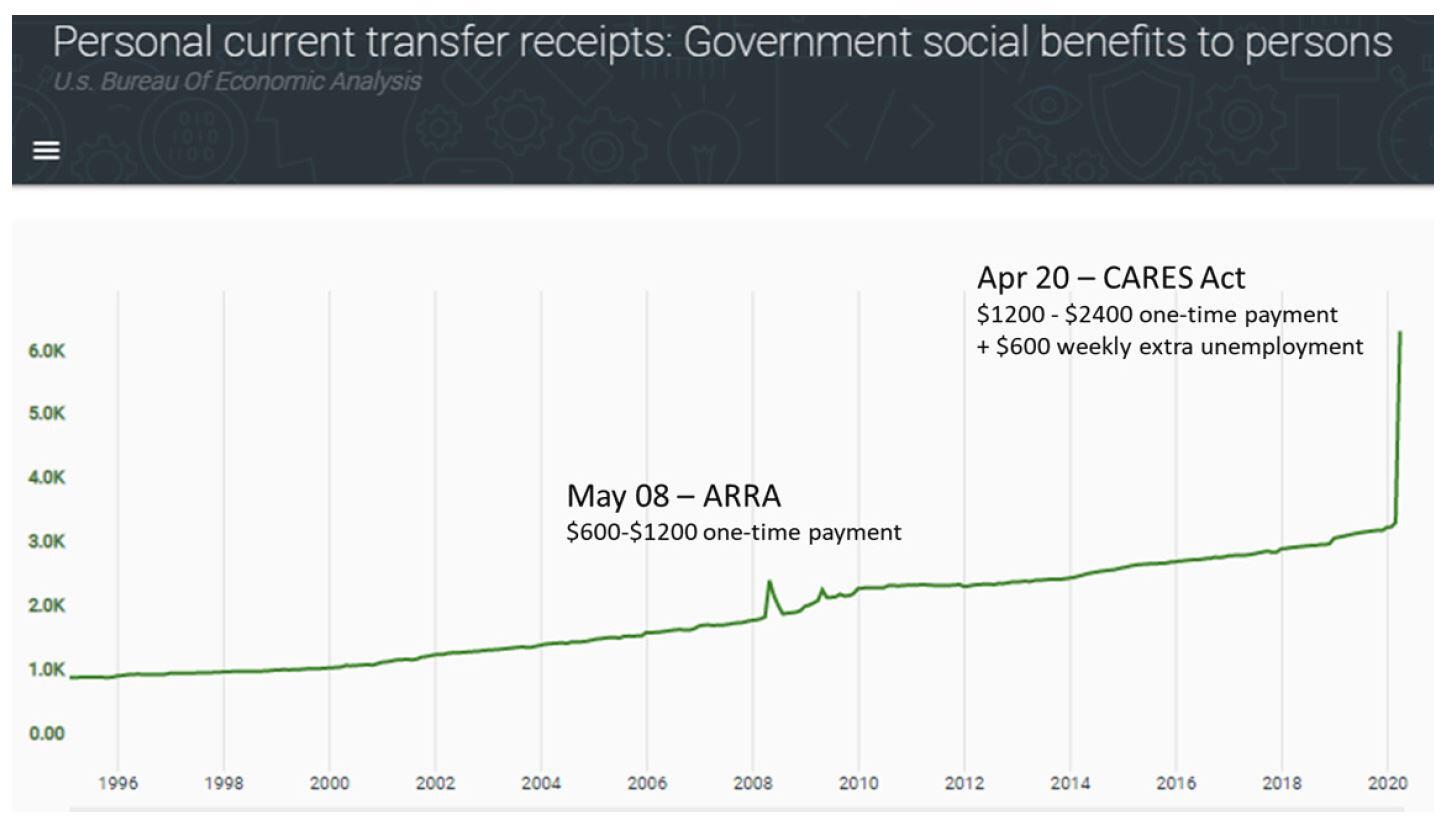

To put that scale in perspective, the following chart shows government social benefits transfers. This is unemployment payments plus any sort of stimulus payments that the government pays out. April 2020, when compared to historical months, is obviously unprecedentedly high.

The American Recovery Act of 2008 was the last time the U.S. had a stimulus, which is illustrated as a little blip in the middle of the chart. At that time, the payments ranged around $600 per person or $1,200 per household. Those numbers were doubled for the one-time payments in the 2020 Cares Act. In addition, there is $600 extra in weekly unemployment that the federal government is providing into state unemployment levels. That is a substantial government transfer that has never been seen before.

Essentially these government actions have boosted real incomes across the United States when you look at measures of incomes. Even though there have been record job losses, the extra unemployment benefit has replaced the median wage. That’s how the government settled on $600 per week. They looked at the gap between average wages being paid out and what states were contributing to unemployment and decided to fill that gap for the average worker.

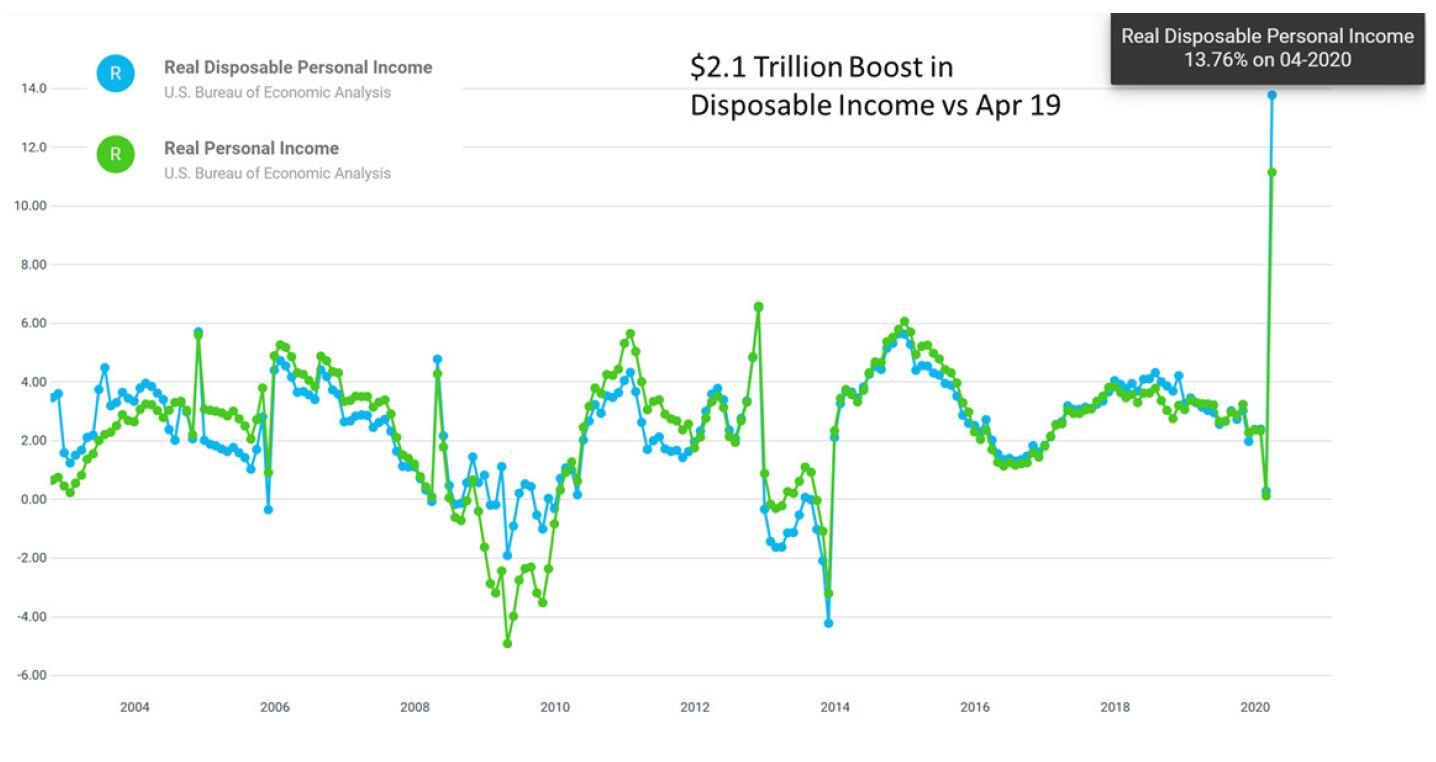

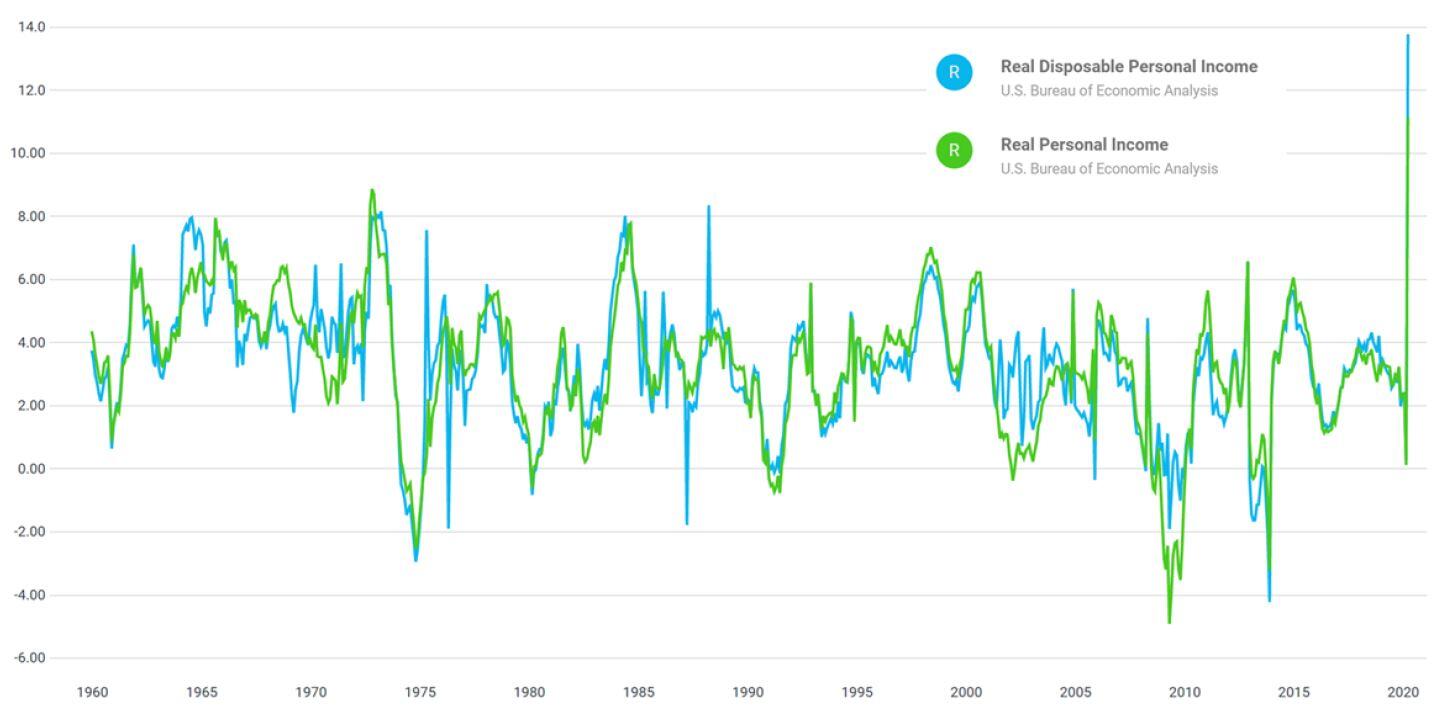

An increase in unemployment benefits and the generous $1,200 to $2,400 in one-time payments means that there is an unprecedented boost in incomes. The following chart shows, in green, the real personal income, and the blue line represents real disposable personal income. The difference between the two is taxes. Disposable personal income is the amount of income left after taxes. Real personal income got a big boost in April and surprisingly went up to the tune of around 11% on a yearover-year basis as indicated in the chart.

If you take into consideration that the stimulus checks are tax free, plus the fact that there are some employer tax breaks, someone who is self-employed may get a generous break from some of the taxes that they would normally pay on the employer side of the FICA taxes.

Real disposable personal income is up tremendously, totaling over a $2 trillion boost in total disposal income versus last year alone with a substantial increase on a year-over-year basis. Considering the extra boost from the tax-free stimulus and employer tax breaks that benefit the self-employed, that’s approximately an additional $300-$400 billion in the gap.

In the following chart, you can see the strong impact in 2020. In 2008 and 2009, stimulus checks only helped compensate for some decline in income, pushing income back to only 2006 levels.

What was just a blip on the chart during the last recession with the stimulus, is not so this time. There was an income decline in March, but the rise in April—when the stimulus came in—was comparably more substantial. Having never seen anything like this before is why it’s been so difficult to forecast industry by industry, category by category.

For businesses able to stay open during this pandemic because they have a product that people might want or need in a social distancing manner, the stimulus has provided consumers the money to spend at these companies, at least right now. Although there have been boosts—you can see all the way back to the 1960s—we haven’t seen this kind of substantial increase in incomes on a year-over-year basis ever.

This stimulus has been very aggressive by historic standards here in the US. Now obviously the $1,200 and $2,400 checks are one-time payments—they won’t show up again and again in May and June and July unless there happens to be a new stimulus that’s passed.

The other part of the stimulus package is the $600 a week in unemployment benefits, which we know for half of Americans will replace, along with the state unemployment, as much, if not more, of the income from the job that they lost. We are seeing a delayed unemployment effect on the economy, with the end of July as the mark when things will change.

In summary, we have a one-time stimulus. There won’t be more $1,200 checks unless a new government stimulus package is passed, which could happen. But the $600 weekly boost to unemployment expires at the end of July, and there will be about 30 to 40 million people to get back to work. If people can’t get back to work, they’re going to be negatively impacted when that $600 goes away unless Congress passes another stimulus measure. But for now, June and July might feel okay depending on what industry you’re in because generally incomes have been replaced and they’ve been replaced plus some.

Looking further, we see that a lot of the stimulus is going into savings. Total spending numbers there are down in March/April, and that confirms that people are saving more. They’re saving substantial portions of the money that comes in, and that’s not necessarily a bad thing.

Savings put people in a better financial position heading into the second half of the year. However, we need to consider delayed effects. The stimulus may be putting incomes well above earnings prior to COVID, to the tune of an unprecedented jump from last year. This effect shows another side to things. We need to consider what happens when the stimulus runs out and people try to transition back into the workforce. We’ve talked about a summer of cautious optimism. Pieces will need to fall into place for people to get back to work and be re-employed and be able to adapt to the new economy.

What’s Ahead: Summer 2020

It’s promising to see businesses reopening. Hopefully social distancing measures will still be encouraged to get the COVID cases to come down. However, caution must be emphasized because what we’ve seen is that the number of cases in the US has almost flatlined over the last few weeks. The number is oscillating around a level that isn’t necessarily dipping lower. And if that continues, we might be in a position where we have to have further restrictions or businesses and other establishments that were going to reopen might have to pull back again.

There could be a danger as we look at the second half of the year. When the weather starts to turn colder there could be more crises as coronavirus is paired with flu season. The combination of health crises impacts and our man-made impacts and problems, such as stimulus running out further compounds possible problems. And what happens after July 31st when those $600 weekly payments expire?

We will be continuing to monitor the influences we’ve mentioned with an expectation in our outlook for a slow recovery to extend into 2021. However, I want to emphasize there’s still a wide range of possible outcomes. As we get more comfortable in this new world, it might be easy to sit back and start to think that the range of possibilities has narrowed a bit. But I think they’re still pretty wide, at least by historic standards. A number of outcomes could happen. We still have a most probable outcome, and that’s the one we have continued to share with you. But I think with the number of new cases over the last few days, there’s still a range of possible outcomes.

In the near term, the boost to personal incomes is benefiting a lot of businesses and also individuals, but we know that that’s not going to last and there’s likely going to be some painful transitions in the future days. That’s something we will continue to keep an eye on.

Economic Scenario Planning in a COVID-19 World

Planning and forecasting based on historical performance is no longer valid in today’s economic climate. As you look ahead beyond the immediate crisis and consider your business plans, having visibility to external economic factors and being able to consider how your company will fare in the “new normal” economy are paramount. This is what we call Intelligent Forecasting.

Prevedere helps companies answer, “what’s next?”, using global data and AI technology.

Whether it is a black swan event like the COVID-19 pandemic, less severe shocks like falling oil prices, or the regular contraction-expansion business cycles, Prevedere provides executives with insights on global forces impacting their business.