Last Updated: January 27, 2021

By Hiram Foster, Full-Stack Data Scientist at Prevedere, The Manufacturing Purchasing Manager’s Index (PMI), Red Herring or Reliable Indicator?

***

red herring | ˈˌred ˈheriNG | noun

Something, especially a clue, that is or is intended to be misleading or distracting.

***

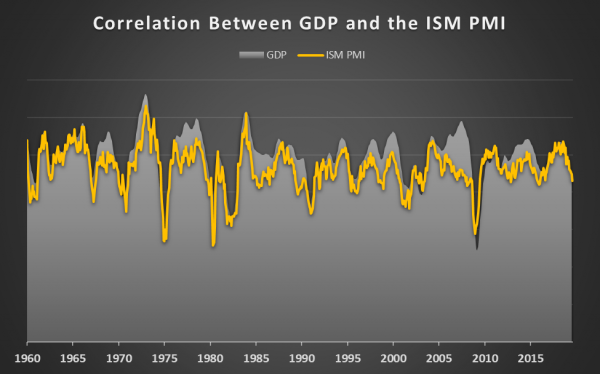

Historically, the PMI (Manufacturing Purchasing Manager’s Index) has proven to be strongly correlated with economic growth and recessionary periods in the economy. Nearly a year before the Great Recession in 2008, the PMI crossed into contraction territory. This September, the PMI was 49.1, the first reported contraction in more than three years. Articles about the “R-Word” and impending doom flooded my newsfeed.

Is the PMI really the canary in the coal mine that is telling us we’re headed into a recession? Or it is a red herring, distracting us from other indicators that might be telling us a different story?

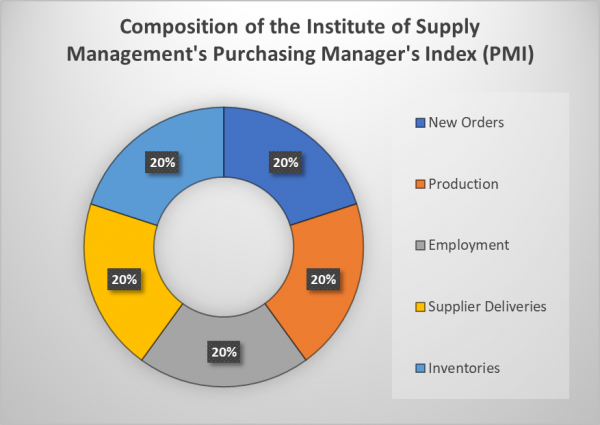

The Manufacturing Purchasing Manager’s Index, or PMI, is the result of a survey of over 300 domestic manufacturers conducted by the Institute of Supply Management (ISM). The answers provided by manufacturing managers and executives are compiled to create an ‘index’ that indicates whether the industry is growing, stagnant, or contracting. A PMI of 50 indicates no growth, and over or under 50 represents growth or contraction in the manufacturing economy, respectively.

An Isolated Recession

Let’s examine what happened three years ago, the previous time the PMI entered contraction territory to better understand the landscape. The PMI hit 48 in December 2015, preceding a major industry slowdown in 2016. According to the New York Times, it was “the most important least-noticed economic event of the decade.”

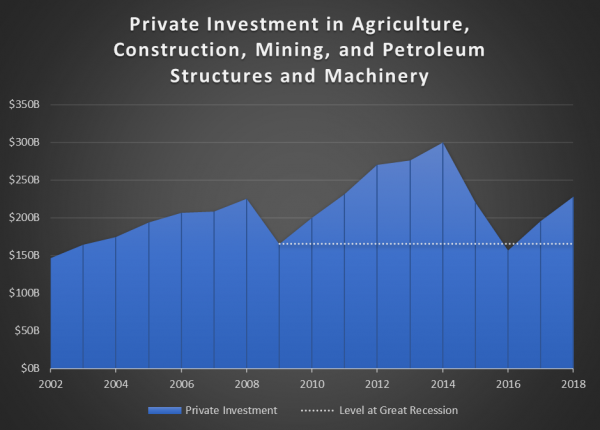

Additionally, manufacturing orders in 2015 were 500 billion dollars less than in 2014. Private investment in the agriculture, construction, mining, and petroleum industries dropped 80 billion dollars and another 63 billion in 2016. The recession in these industries was more severe than they experienced in 2009.

Interestingly, this slowdown didn’t lead to a full-fledged recession. You likely didn’t hear that manufacturing lost over 30,000 employees in the 2nd half of 2016, the equivalent of 20 Lordstown GM plants. Why didn’t this make the headlines? The rest of the economy barely noticed; consumer spending and GDP were still strong, and the ISM PMI returned to growth territory.

A Changing Economy

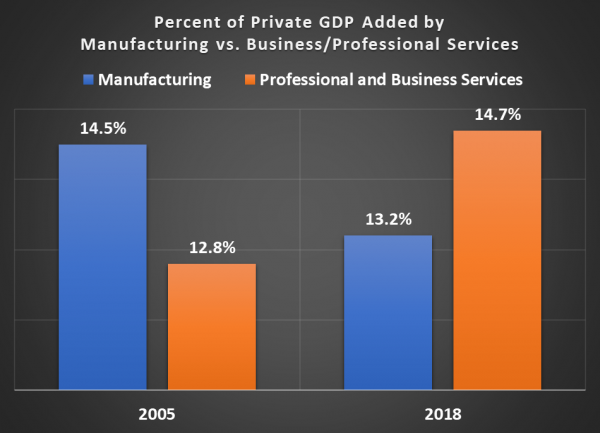

In 2005, manufacturing contributed 1.9 trillion dollars to US GDP, or in other terms, 15% of the total value contributed by private industries.[1] In Q1 of 2019, that contribution dropped to 13%. It might seem like a small difference, but it’s a difference of nearly 230 billion dollars. Put another way, the value added by the manufacturing sector has shrunk by more than 10 times

In the same time period, the private sector still grew by 3.7 trillion dollars between 2005 and 2019. If not manufacturing, what fueled that growth?

The GDP that used to come from manufacturing has been replaced by what the government calls “Professional and Business Services.” Jobs that “require a high degree of expertise and training” have been steadily displacing manufacturing’s place in the economy over the past fifteen years. Today, Professional and Business Services now contribute to the economy more than manufacturing did in 2005.

In the past, the PMI has provided a reliable signal of our economic health, sometimes even foreshadowing recessions long before the rest of the economy noticed. However, growth in the services sector, as well as increased automation and globalization, have significantly reduced the correlation between the manufacturing sector and the rest of the U.S. economy. The manufacturing industry may be contracting, but other indicators are poised to share PMI’s crown and prove themselves to be suited for evaluating the health and future of our 21st-century economy.

————————————————————————————————————

Hiram Foster is a Full-Stack Data Scientist at Prevedere, leveraging bleeding-edge data science tools to reveal actionable insights for Fortune 1000 businesses. He holds a B.Sc. from Ohio University’s Honors Tutorial College and is a graduate of Microsoft’s Professional Program in Data Science. A startup enthusiast, Hiram previously led business intelligence initiatives at Bold Penguin, a commercial insurance software solution.

[1] All GDP numbers are adjusted for inflation (i.e. “Real Value Added”).